Deep Dive: Intuit (INTU)

When is it suitable to try and catch a falling knife?

In April, I released my Deep Dive into the UK-listed small-to-medium-business (SMB) tax and Human Resources (HR) management software company, Sage. As part of that exercise, I briefly reviewed a number of their competitors, including Intuit INTU 0.00%↑, and I generally liked what I saw from the fundamentals. After releasing their 2026 3rd-Quarter (26Q3) results on 20th May, INTU stock has plummeted from approximately $400 per share, to a price at the time of writing of $267 per share. Does this mean the stock is now attractively priced, or is the brutal drop a foreboding sign of future difficulties to come?

Let’s dive in!

DISCLAIMER: I am not a financial advisor. Nothing I say should be construed as financial advice or as a recommendation to buy or sell a stock. At the time of writing, I am a shareholder of Intuit Inc. I undertake my own analyses and, although I take efforts to ensure my analyses are reasonable, I cannot guarantee their accuracy. I may have interpreted information incorrectly or made certain assumptions that are different to management and other investors. Please do your own research and seek advice from a registered financial advisor before deciding whether or not to invest.

Contents

Who are Intuit, Inc.?

Product Offering

Executive Leadership

Board of Directors

Stock-Based Compensation

Mergers and Acquisitions

Revenue and Operating Profits

By segment

Total

Working Capital and Debt

Return on Capital

Earnings and Free Cash Flow

Dividends

Risks

Valuations

Conclusions

Who are Intuit, Inc.?

Intuit’s mission is “powering prosperity around the world”, where they aim to “[give] everyone the opportunity to prosper… and [never stop] working to find ways to make that possible.” They are in essence a fintech company, with a portfolio of products intended to help individuals and small companies manage their businesses, personal tax and credit exposure.

Their portfolio consists of 4 main products:

QuickBooks

TurboTax

CreditKarma

Mailchimp

In addition, Intuit have an “Enterprise Suite” product, which helps with the management of Groups of companies, including inter-company transactions. Lastly, Intuit offers a Business Credit Card product, sync’d with QuickBooks.

Intuit recently changed its segment reporting, and now reports across two key segments, Global Business Solutions and Consumer segments. Global Business Solutions is essentially Intuit’s QuickBooks, Enterprise Suite and Mailchimp products, across both Online and Desktop environments, while its Consumer segment consists of TurboTax, Credit Karma and ProTax products (ProTax being intended for accountants). Below, I will step through each of Intuit’s 4 main products.

QuickBooks

QuickBooks is Intuit’s core business management software, with products aimed at price points appropriate for sole traders, small businesses, medium businesses and accountants. Excluding various deals and offers, QuickBooks has offerings priced from £10/month to £123/month. The main features at each price point are laid out below (from a UK-perspective):

Sole Trader Plus. £10/month, intended for non-VAT-registered traders. Supports the UK’s “Making Tax Digital” directive, provides receipt capture, mileage tracking and invoicing, with automated bank feeds and AI-powered Intuit Intelligence chat.

Simple Start. £16/month, intended for VAT-registered sole traders. In addition to the Sole Trader Plus offering, this tier provides AI-supported VAT management and submission to HMRC, and provides the option to add on payroll management.

Essentials. £38/month for up to 3 users. Adds support for multiple currencies, cashflow planning, bill management and recurring invoices, plus the ability to log employee time, add customer referrals, feedback and testimonials, customer requests and sales lead tracking, schedule meetings with customers and provides an AI assistant to spot and help reconcile transactions requiring attention. In addition, there is a small level of customisation permitted.

Plus. £56/month, adds project management and profitability tools, budgeting and inventory management, purchase and sales orders and permits for contract upload and e-signatures. This tier also allows a much higher level of customisation.

Advanced. This is QuickBooks’ top tier, priced at £123/month. Adds AI tools for finance and project management, plus automated revenue recognition and tracking of fixed assets, as well as adding forecasting and custom reporting tools. This tier provides premium support, backup and restore functions and allows for workflow automation and batching of invoice and expenses.

QuickBooks also has products for accountants, priced from a free offering to £69/month. The higher tier permits a greater number of AI prompts, with AI-powered anomaly detection, customisable dashboards, client groups and cross-client comparisons. Accountant partners can also secure QuickBooks products for their customers at a 50% discount.

QuickBooks offers three levels of payroll support, from “Core” to “Premium” and “Elite” tiers. All three tiers are UK HMRC-recognised, allowing PAYE (Pay-As-You-Earn) taxes to be reported online, with automated calculations, tax code updates and automated payroll runs on weekly, fortnightly, 4-weekly and monthly bases, including statutory pay calculations and pension contributions. The higher tiers also provide for shift scheduling, with the Elite tier permitting project-based collaboration and detailed reports for project tracking.

TurboTax

This product is definitely intended for North American consumers and those having to file their own taxes. This is unusual in the UK, where most people have simple income-based tax arrangements that are automatically managed and calculated by HMRC via PAYE arrangements.

TurboTax for individuals and families has three main tiers: their Do-It-Yourself (DIY) tier, priced at $0 - $139; their Expert Assist tier, priced at $59 - $209; and their Expert Full Service, priced from $129. In all cases, Intuit provides a guarantee of 100% accurate calculations. Within the Do-It-Yourself and Expert Assist tiers, there are Basic, Deluxe and Premium options, with the basic tiers supporting education expenses and student loan payments, income tax credits and child tax credits, while intermediate tiers help customers to find appropriate deductions, manage charitable contributions, mortgage interest and property taxes as well. Higher tiers also offer support for investment options, including rents and depreciation, employee stock options and crypto currencies. All tiers are guaranteed by Intuit to maximise tax savings for customers. This is significant in the current AI-enabled environment.

TurboTax also offers Expert Assist for businesses, with a Sole Proprietor offering for $239, and S-corp (a U.S. business model that permits pass-through of profits and losses to an individual without double-taxation) and Partnerships priced from $639. Their Expert Full Service for Sole Proprietors is priced at $259, with their S-Corp and Partnerships Full Service offering priced at $1,549.

TurboTax aims to match customers with tax experts who specialise in that customer’s industry to help maximise credits and deductions.

Credit Karma

Credit Karma is a personal finance product enabling customers to shop for credit cards, personal loans, car loans, mortgages, insurance and refinancing options. At its essence, Credit Karma operates as a marketplace, enabling potential customers to search and compare product offerings from suppliers. In addition, it also provides customers with a means to build up their credit score via their Credit Builder and Credit Spark products, which link to customer bank accounts and open lines of credit in the customer’s name with Credit Karma’s banking partner, enabling customers to pay their bills and improve their credit scores by demonstrating on-time payments and providing for automated credit payments into a savings account, backed by payments taken from the customer’s external bank account each month.

Intuit have recently restructured their segments to bring TurboTax and Credit Karma together under their Consumer segment. In their 26Q3 earnings call, [CEO] Sasan Goodarzi stated that Intuit sees 30% higher revenue per user for customers using both TurboTax and Credit Karma products, compared to customers using TurboTax alone.

Mailchimp

Mailchimp provides a direct marketing and analytics platform to its customers, with automated workflows and templates to build personalised marketing campaigns across email and SMS, providing customer and market research tools. Mailchimp is making heavy use of AI tools to track and analyse performance of marketing campaigns, with a claimed 30x Return on Investment for its users with e-commerce stores linked to Mailchimp accounts.

Mailchimp offers email marketing products at three price tiers. The initial offering is free for customers with less than 250 contacts. The Essentials tier starts at £9.80/month, the Standard tier costs from £15.08/month, and the Premium tier costs from £263.94/month. All tiers offer a 15% discount for accounts with more than 10,000 contacts, but the monthly cost also increases and the number of contacts increases as the number of contacts increases. The Essentials tier tops out at £290.34/month for up to 50,000 contacts, while the Standard tier tops out at £603.30/month for up to 100,000 contacts. At 150,000 contacts, the Premium tier costs over £1,200/month. Above 200,000 contacts, the product becomes bespoke. Adding SMS marketing increases the cost of the Essentials package to £24.88/month at the low end, while it doesn’t cost anything extra at the very top end of the Premium offering.

The main differences in the product offerings across the tiers lie in the customisation and use of templates and reports, the number of discrete audience groups and the number of emails that can be created or sent per month. The higher tiers also enable A/B testing, social media posting, time-zone-dependent delivery, behavioural targeting and ad re-targeting with Google, as well as offering advanced and predictive segmentation tools.

Mailchimp also offers a transaction-based business model, allowing customers to buy credits for blocks of emails.

Executive Leadership

Named Executive Officers

Intuit’s 2025 Proxy Statement has 5 named executive officers (NEOs), while their website lists 12 members of their Executive Team. The five NEOs are profiled below.

Sasan Goodarzi became CEO in 2019, having previously led Intuit’s consumer group and global business solutions group. Goodarzi has been Intuit’s Chief Information Officer and General Manager of Intuit’s ProTax organisation and was also General Manager of the Financial Services division. Prior to his career at Intuit, Goodarzi worked as global president of the products group for Invensys and held leadership positions within Honeywell’s automation control division. Goodarzi was also co-founder and CEO of tech startup Lazer Cables.

Sandeep Aujla joined Intuit in 2015 and is currently Chief Financial Officer, having previously served as Senior Vice President for Intuit’s Small Business & Self-Employed Group and their Technology Finance organisation. Before joining Intuit, Aujla worked in finance, previously working for Visa and having held investment banking roles with Goldman Sachs and Morgan Stanley.

Alex Balazs is Executive Vice President and Chief Technology Officer, having started in Intuit as a software developer in 1999 and, as Chief Architect, developing Intuit’s generative AI operating system, GenOS. Before working for Intuit, Balazs held engineering roles with ZEISS Medical Technologies and Light Lab Imaging.

Mark Notarainni is Executive Vice President and General Manager of Intuit’s Consumer Group, leading the TurboTax and Credit Karma organisations. Notarainni joined Intuit in 2009 as leader of the Customer Success organisation, having previously worked for NCR Corp., Dell and Hewlett-Packard.

Marianna Tessei was Executive Vice President and General Manager of Intuit’s Small Business Group, but stepped down at the end of May 20261. Ashley Still has now assumed responsibility for this Group, expanding her role to become Executive Vice President and General Manager of the Small Business and Mid-Market Group. Still now leads the organisations providing QuickBooks and Enterprise Suite, also covering their Accountant and Partner offerings. Prior to joining Intuit, Still spent 20 years at Adobe, leading their Document Cloud and Creative Cloud businesses.

In addition, Intuit’s 2025 10-K names Anton Hanebrink, Caryl Hilliard, Kerry McLean and Lauren Hotz as Executive Officers. Hanebrink joined Intuit in 2016, having previously worked in venture capital and corporate strategy, with time served at Boston Consulting Group, Hewlett-Packard, Opus Capital and Block. Hilliard has been with Intuit for 27 years. McLean is General Counsel and has been with Intuit since 2006, having previously worked for various legal firms. Hotz joined Intuit in 2004, having previously worked for accountancy firms and other public companies, including time served with a firm that is now PwC. In short, a lot of Intuit’s executive leadership has been with the company for a long time, so can be assumed to understand the company and its culture well.

2025’s Executive Compensation was 95% performance-based. There are only small differences between the CEO’s compensation and that of other NEOs, so I’ll use the CEO’s compensation as my reference. In 2025, executive compensation consisted of:

4% base salary, with Goodarzi taking a salary of $1.3M

7% incentive cash, with Goodarzi receiving $2.6M

43% Performance Stock Units (PSUs), with Goodarzi receiving stock valued at $15.6M

23% Restricted Stock Units (RSUs), with Goodarzi receiving stock valued at $8.7M

23% stock options, with Goodarzi receiving options valued at $8.7M

In aggregate, Goodarzi received compensation of $37M in 2025. Executive directors are expected to hold stock worth ten times their base salary. Long-term incentives are set up to be nominally 50% PSUs, to vest over a 3-year period, 25% RSUs, to vest over a 4-year period, and 25% stock options with a 7-year life.

The cash bonus is set up to be weighted 50% on revenue targets and 50% non-GAAP operating income, with a maximum payout of 150% of target. In 2025, the bonus paid out at 115.1% of revenue target and 120.5% of operating income, for a total payout of just under 118%. I am personally glad to see the bonus is not per-share and that it is based on revenue and operating income, meaning it is driven by customer willingness to pay and operating performance, although I believe using “adjusted” operating profit still provides management with opportunity to influence the metric for personal gain. Adjustments like Stock-Based Compensation (SBC) and restructuring costs should be included in the metric, in my opinion.

Long-term incentive PSUs are based on Intuit’s Total Shareholder Return (TSR) percentile rank within a peer group of 43 companies, with 100% payout being based on achieving at least 60th percentile (although 2025 paid out at 102% of target for a 58th percentile rank). The peer group includes: some of the S&P technology companies like Google, Meta, Microsoft and Apple; Computer hardware and semiconductor companies like Dell, HP, Cisco, Cadence Design, Broadcom and Qualcomm; payments companies like Block, Mastercard, Visa, PayPal and Sea Ltd; games companies like Electronic Arts and Take-Two; Cyber security companies like Fortinet, Crowdstrike and Palo Alto Networks; and some more obvious peers like Salesforce, SAP, ServiceNow and Workday. Then there are other software-as-a-service companies like AirB&B, AppLovin, Atlassian, Baidu, Netflix, Palantir, Uber and some more unusual peers like Super Micro Computer and Autodesk. Personally, I see very little commonality across the peer group and I’m not sure why they have all been selected. I would prefer to see a more focussed set of peers, or explicit justification for each.

Board of Directors

From their November 2025 Proxy Statement, Intuit’s Board of Directors has an average tenure of 9 years and a median of 7 years, with one director being below 50, 5 directors being 50 - 60 years old and 5 directors being over 61. Of the 11 Directors, 9 are classed as independent, and two are non-independent.

The non-independent directors are Sasan Goodarzi, as CEO and Chairman, and founder Scott Cook, who has been Director since 1984! Cook was CEO until 1994, and has previously been a Director of Proctor & Gamble and of eBay. Intuit have only recently combined their Chairman and CEO roles, having had separate individuals in each role previously.

Independent directors are:

Vasant Prabhu, Lead Independent Director and former CFO and Vice Chairman of Visa, Inc. Prabhu has prior experience working for NBCUniversal, Starwood Hotels & Resorts, Safeway, McGraw-Hill and PepsiCo.

Eve Burton, Executive Vice President and Chief Legal Officer of lifestyle media and publishing house, The Hearst Corporation

Richard Dalzell, former Senior Vice President and Chief Information Officer of Amazon, previously working for Walmart and a director of AOL.com and Twilio.

Thomas Szkutak, former Senior Vice President and CFO of Amazon, formerly of General Electric, with previous private equity experience.

Deborah Liu, former President and CEO of Ancestry.com, former Vice President of Facebook / Meta Platforms

Tekedra Mawakana, Co-CEO of Waymo and formerly VP for eBay and Yahoo!

Forrest Norrad, Executive Vice President of Data Center Solutions Business Group for Advanced Micro Devices, with previous experience working for Dell

Raul Vazquez, who stepped down as CEO of NASDAQ-listed fintech company, Oportun Financial, in January 20262. Before his time at Oportun, Vazquez worked for Walmart. and he has a background with e-commerce startups.

Eric Yuan, Founder and CEO of Zoom Video Communications, formerly of Cisco and a founding engineer of Webex, before it was acquired by Cisco.

In the same Proxy Statement, Intuit revealed they would be appointing two new directors in August 2026, Adena Friedman (Chair and CEO of the NASDAQ stock exchange and B Director of the Federal Reserve Bank of New York) and Bill McDermott (Chair and CEO of ServiceNow, formerly CEO of SAP America).

Reviewing their CVs, I was struck by how many of the Board had engineering backgrounds, and often not software engineering - electrical engineering, civil engineering, industrial engineering and mechanical engineering are all represented. I was also pleasantly surprised by how many of the executive leadership team were female - of the 12 executive leaders listed on Intuit’s website, one third are female.

Independent directors are paid a retainer of $75k in cash, which can be deferred into stock, and $280k in equity, deferred for 5 years from vesting. Meanwhile the Chair of the Board is paid a cash retainer of $90k, committee members are paid $10k - $20k, and committee Chairs are paid a further $17.5k - $32.5k. Directors are required to hold Intuit stock worth 10 times their annual cash retainer, with the ownership threshold to be achieved within 5 years of becoming a Director. Executive directors are required to hold 10 times their base salary.

In 2025, non-employee director compensation varied from $380k to $580k. This compares to a total compensation of $242k for Intuit’s median employee, based on an employee population of 17,335 according to their November 2025 Proxy Statement. In their July 2025 Annual Report, Intuit declared they paid $300M in staffing costs and had approximately 18,200 employees, indicating an average cost of $16.5k per employee. However, Intuit also recorded $1.4 bn in share-based compensation expense in 2025, which works out at $78k per employee on average. Therefore, the average employee in July 2025 received around $95k compensation, vs. the declared median employee total compensation of $242k in November 2025.

Stock-Based Compensation

I wouldn’t normally introduce stock-based compensation so early in a research article, but I think it is warranted in this case, given the high level of employee and director compensation paid via equity.

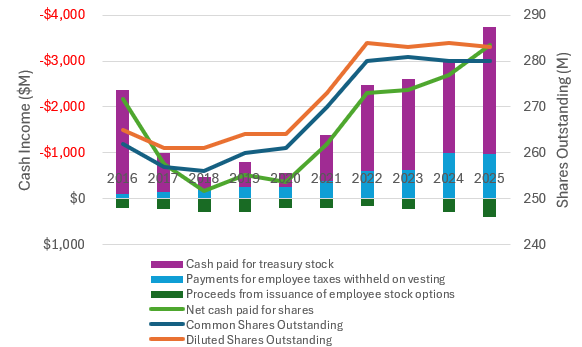

Intuit issues several million restricted stock units and stock options each year, and manages its shares outstanding through open market re-purchases to replenish its treasury stock.

There are three main stock-based cash expenses: the money Intuit receives from its employees for any stock options exercised; tax paid by the company on behalf of its employees; and money paid by Intuit to purchase shares on the open market. Intuit has been paying increasing amounts of money each year for both purchases of treasury stock and payment of taxes due. Share count rose rapidly from around 260M shares outstanding in 2016/17 to 280M in 2022. Since 2022, the net cost to Intuit rose from $2.3 bn to a little over $3 bn by the end of the 2025 fiscal year, in order to hold share count approximately constant.

SBC is accounted for with stochastic models that estimate the value being granted via share awards, considering the risk-free interest rate, the expected dividend yield and the expected share price volatility. However, another way of assessing the cost to the company of its SBC is to look at the net cash spent each year.

Intuit receives cash from its employees when stock options are exercised, but it then re-purchases shares on the open market to hold in treasury to maintain its share count, and pays tax liabilities related to stock options and equity issuance to employees.

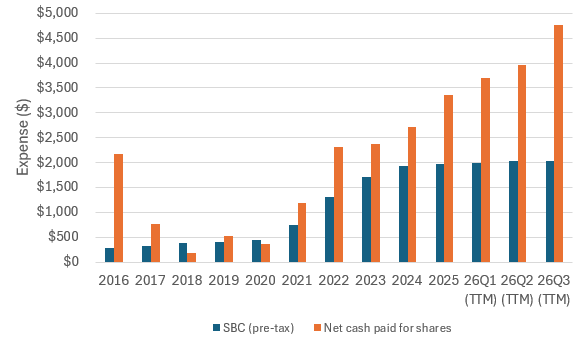

With this view, the figure below shows that Intuit’s SBC accounting expense typically underestimates the total cost of its SBC policy, and the difference between the accounted cost and the net cash cost is increasing each quarter. This means an adjustment to operating cash flow and free cash flow will be required to account for SBC, as the non-cash SBC expense recorded in operating cash flow is inadequate to fully account for the cost of holding Intuit’s share count constant.

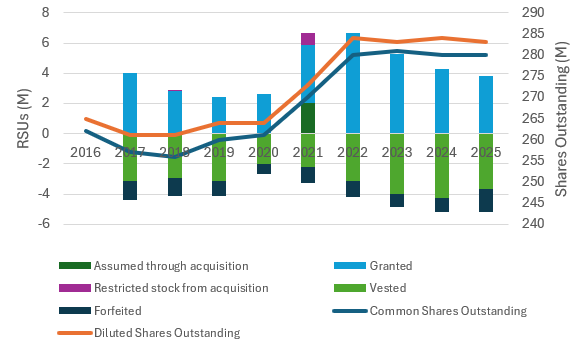

Although there was a period just before COVID when share issuance was lower, in general Intuit grants 4 - 5 million shares per year, with a similar amount being vested and a small amount forfeited or expiring each year. Granting or vesting around 4M shares per year on a total number of shares outstanding of around 280M implies a roughly 1% - 2% stock dilution headwind each year.

Mergers and Acquisitions

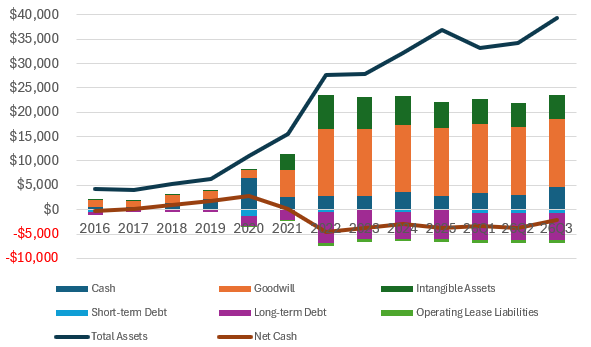

Since 2016, Intuit have made two major acquisitions - Credit Karma in 2020 and Mailchimp in 2021. In both cases, Intuit closed the deals with a mix of cash and equity. There were also a number of smaller transactions in 2018. Mailchimp was the larger of the two, bought for $12 bn total consideration, consisting of $5.7 bn in cash (mostly funded by debt) and 10.1M in shares, valued at $6.3 bn. Credit Karma was bought for $7.2 bn using $3.4 bn of cash and 10.6M shares, worth $3.8 bn. The 20.7M shares transferred as part of the total consideration for these two acquisitions accounts for the vast majority of the increase in share count between 2020 and 2022.

Mailchimp added around $8.1 bn to the goodwill on Intuit’s balance sheet, while Credit Karma added $3.9 bn.

These acquisitions caused a step change in goodwill in 2021 and in both goodwill and total debt in 2022. At that time, goodwill accounted for almost half of total assets and combined goodwill and intangible assets accounted for three quarters of total assets. However, since those large acquisitions, goodwill has remained stable in absolute value and intangible assets have reduced in value through amortisation, while Intuit’s total assets have increased. Cash has grown from around $3 bn to almost $5 bn, while debt has remained fairly constant at around $5 bn, meaning net debt has decreased from almost $5 bn to $2 bn.

Although goodwill and intangible assets remain a significant portion of Intuit’s balance sheet, it is encouraging that Intuit has not recorded any impairments of goodwill or acquired intangible assets since its 2015 fiscal year.

Revenue and Operating Profit

Having laid out the four key products offered by Intuit (QuickBooks, TurboTax, Credit Karma and Mailchimp), and shown how and when Credit Karma and Mailchimp were acquired, it is instructive to look at how and where Intuit generates revenue, particularly if we wish to assess the relative success of these large acquisitions.

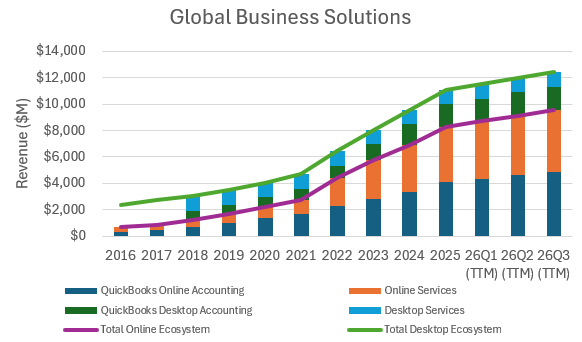

Global Business Solutions

Previously disclosed as Intuit’s “Small Business and Self-Employed” segment, Global Business Solutions is the segment that hosts the QuickBooks product suite (including Enterprise Suite, payroll, time, financing and money management offerings) and Mailchimp. The segment is decomposed into Online and Desktop ecosystems, and Services are separately disclosed. Mailchimp sits within the Online Services part of the segment. Before 2018, I’ve had to infer some of the results from relative changes, as the absolute values have not been disclosed.

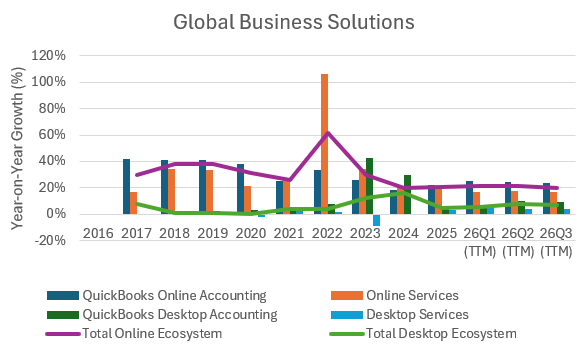

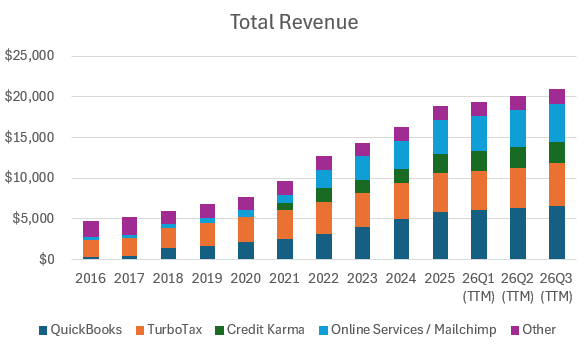

Over the ten years (well, 9.75 years) from 2016 to the 3rd Quarter of 2026 (26Q3, which are the most recently disclosed results), Intuit’s Global Business Solutions segment has exhibited a Compounded Annual Growth Rate (CAGR) of 18.5%. However, within that result, the Desktop Ecosystem has had a CAGR of 5.7%, of which most growth was delivered in 2023 and 2024, when Intuit enacted a licensing change to a recurring subscription revenue model. The Online Ecosystem has provided a CAGR of other 30% since 2016. The Online Ecosystem got a major boost in 2022 from the Mailchimp acquisition, when the Online Services part of the segment doubled in revenue, although the annual growth rate for the Online Ecosystem has since slowed to around 20%.

Within the segment, the split between QuickBooks Accounting and Services is close to 50/50, with the balance having switched from 45/55 in favour of Services in 2018, to nearer 55/45 in favour of QuickBooks by 26Q3. Online has grown from 30% of segment revenue in 2016 to over 75% of segment revenue by 26Q3.

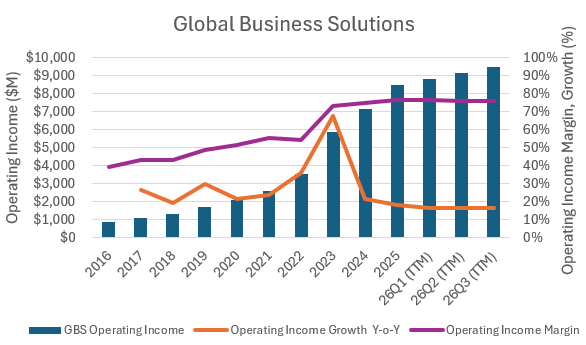

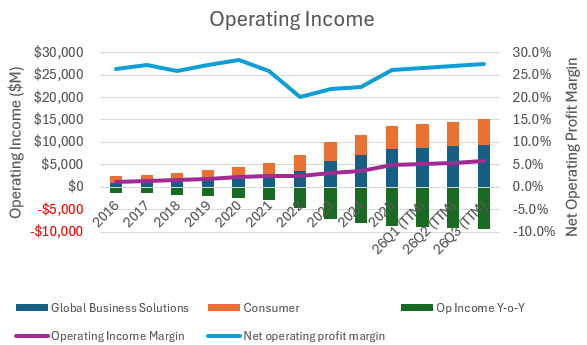

Operating Income for the segment has consistently grown since 2016 with a material change in operating profit margin in 2023, which represented the first full year of Mailchimp’s results. Although the annual growth in operating profit has slowed to around 16%, operating profit margin for the segment has expanded, and is now running at around 76% (although this is before stock-based compensation, due to how Intuit discloses its results).

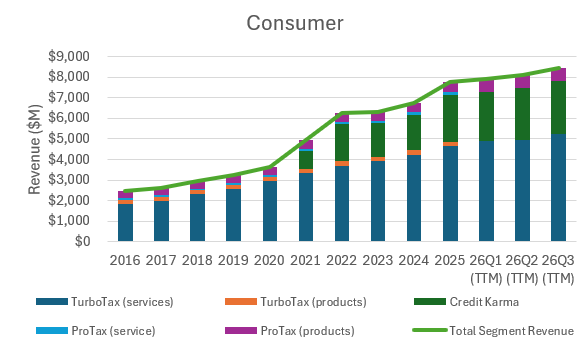

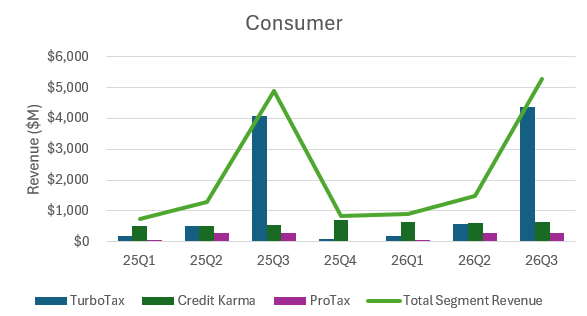

Consumer

For their 2026 quarterly reports, Intuit have rolled TurboTax, Credit Karma and their ProTax products into a single “Consumer” segment, whereas up until their 2025 annual report, “Consumer” was predominantly TurboTax, with Credit Karma and ProTax being disclosed as discrete segments. ProTax was previously known as ProConnect and, before that, as Intuit’s Strategic Partner segment. This is the segment Intuit uses for its products for professional accountants.

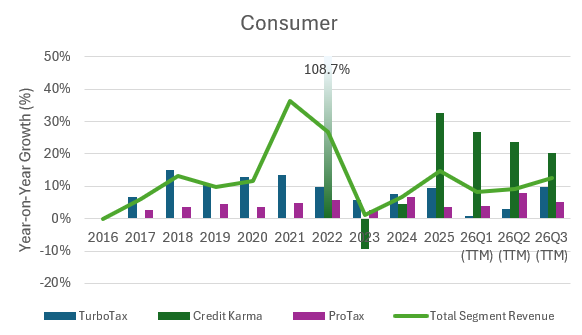

TurboTax is a predominantly services-based segment, whereas Credit Karma is entirely services-based, and ProTax is predominantly product-based revenue. The segment has achieved a CAGR of 13.5% since 2016. Within the segment, TurboTax has achieved a CAGR of 10% and ProTax has achieved a CAGR of 4%. As both existing categories are below the degment average, the difference in segment growth must be down to the inclusion of Credit Karma in 2021. Since 2022 (Credit Karma’s first full year of results), Credit Karma has also achieved a CAGR of 10%.

TurboTax and ProTax are highly seasonal businesses, with tax season running from roughly January until April. This results in the vast majority of TurboTax revenue being recognised in Q3, with some revenue, particularly in the ProTax professional accountant segment, being recognised in Q2.

TurboTax has grown fairly consistently at around 10% per year since 2016, and ProTax has shown relatively stable growth of around 4% - 5% per year, but Credit Karma has been more volatile, with a slight decline in 2023, rapid growth in 2025, and declining growth so far through 2026.

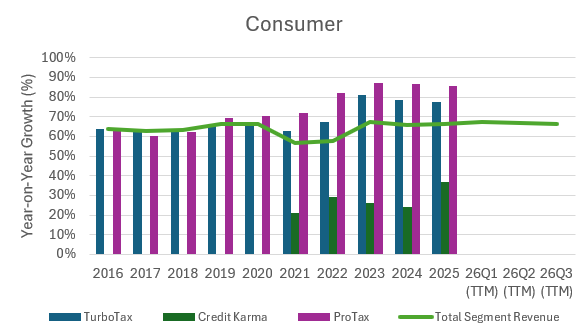

The Consumer segment is a high-margin segment, similar to the Global Business Solutions segment, with margins in the mid-to-high 60 percent range. TurboTax and ProTax margins have been increasing in recent years, reaching around 80% operating profit margin. Credit Karma is relatively low-margin (compared to Intuit’s other products), at less than 40%.

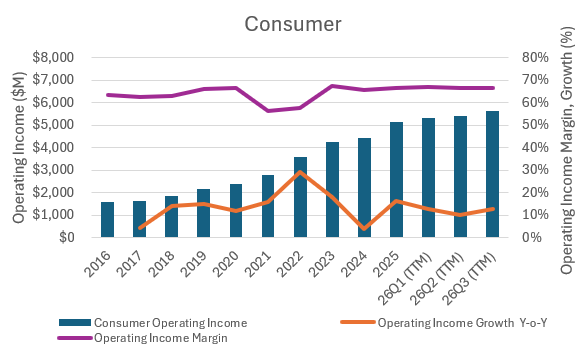

In absolute terms, Intuit has been growing its Consumer operating profit each year, with annual growth typically around 10% or slightly higher.

Total Revenue and Operating Profit

The Global Business Solutions segment is worth about 60% of total revenue, with Consumer making up the other 40%. The product split between QuickBooks, TurboTax, Credit Karma and Online Services (including Mailchimp) is fairly even, with Quickbooks accounting for around 30% of revenue, TurboTax accounting for around 25% of revenue, Online Services being worth 20% - 25% of revenue, Credit Karma contributing around 10% of revenue, with other sources of revenue being worth around 10%.

There are a number of corporate operating expenses that Intuit does not allocate to a segment, most notably SBC, amortisation of technology and acquired intangible items, restructuring charges and “other” corporate expenses. Collectively, these are of a similar magnitude to the segment profits and act to bring the net operating profit down to around 25% - 30%. Net operating profit margin was highest before the Mailchimp and Credit Karma acquisitions, but recent trailing twelve month performance indicates profit margins are returning to previous highs.

Overall, Intuit looks like a company achieving decent annual growth rates of around 15% each year, with consistent, respectable profit margins of over 25% and cash profits that are keeping pace with revenue growth, despite high levels of stock-based compensation.

Working Capital and Debt

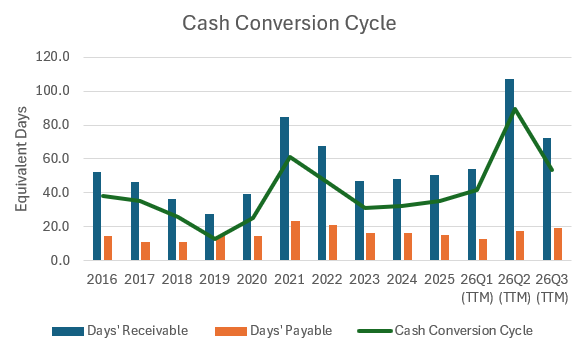

Cash Conversion Cycle

Intuit has no inventory on its balance sheet and has low levels of accounts receivable or payable, which leads to a short cash conversion cycle. The level of receivables fluctuates and is trending up over time, while payables tend to be more consistent. However, Intuit is still able to convert orders into cash within 2 - 3 months, with a cash conversion cycle of around 54 days up until April 2026 (26Q3), having reached a maximum of around 90 days in January 2026 (26Q2).

Debt and Cost of Capital

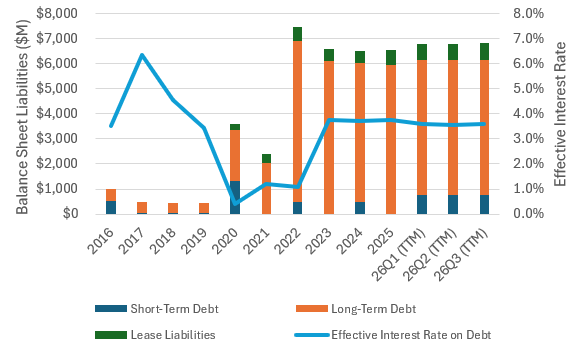

Debt

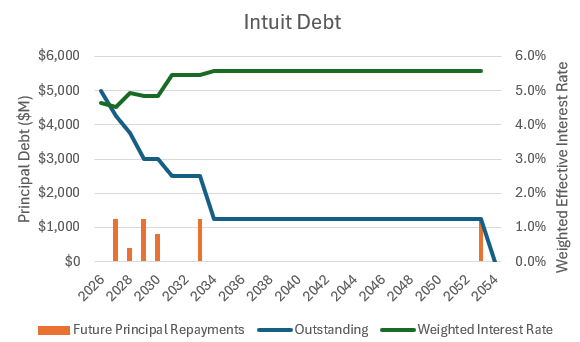

As of April 2026 (26Q3), Intuit had $6.2 bn of debt outstanding, including a $1.2 bn revolving credit facility. For a company that generates $4 bn - $4.5 bn in operating profit after tax, this is a very manageable level of debt. Looking at the maturity profile, a lot of the debt is cleared within 10 years, with a maximum annual principal payment of $1,250M. Beyond the mid-2030s, there is one outstanding $1,250M note, due 2053. As the debt issued in 2020 in a low interest rate environment matures, the effective interest rate will tend towards the approximately 5.5% rate at which the most recent debt has been issued, meaning the effective interest rate will rise from around 4.6% to 5.5% by the mid-2030s.

N.B. I believe there is a minor discrepancy between the maturity dates of Intuit’s notes and the declared future principal payments in their annual reports, so the burndown profile of debt and principal repayments do not fully align in the depiction below. However, I believe the difference is immaterial to the discussion and can be ignored.

From the interest expense incurred on Intuit’s income statement, including lease liabilities, Intuit’s effective cost of debt is lower than the coupon payable on its issued notes. Intuit’s effective cost of debt, based on its interest expense, is around 3.6%.

Cost of Capital

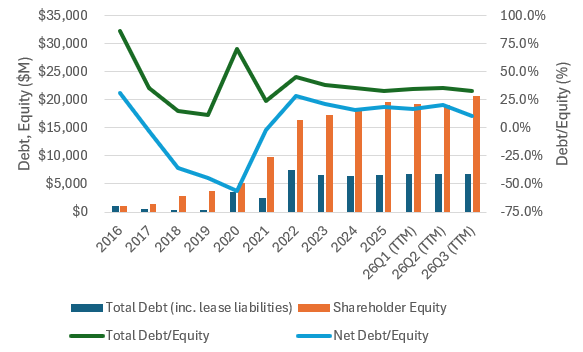

The rapid growth in Intuit equity over the period 2020 - 2023 has permitted Intuit to carry more debt, although its level of debt has been pretty constant since 2023. Although debt/equity spiked in 2020 and increased in general from 2019 until 2022, following the Mailchimp acquisition, debt/equity has generally stayed below 50%. Intuit actually ran a net cash position from 2017 until 2021. Today, debt/equity is around 33% and net debt/equity is down to 10%, indicating debt is only a small part of Intuit’s capital structure.

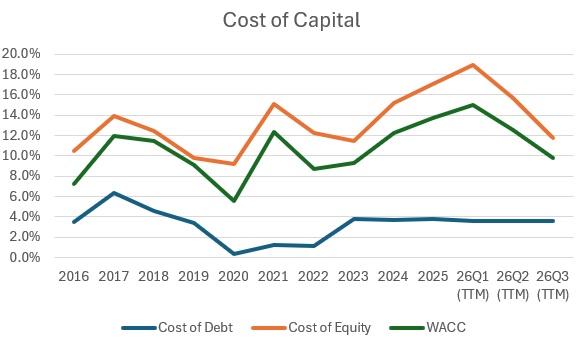

Using the Capital Asset Pricing Model (CAPM), a cost of equity can be estimated based on the correlation of Intuit’s share price to the performance of the S&P 500 index. Using the Beta correlation coefficient quoted by Zacks and trailing 5-year S&P 500 performance, I have calculated a cost of equity for Intuit to lie between 9% and 18%, sitting around 14% on average.

Combining the cost of debt and the cost of equity into a Weighted Average Cost of Capital (WACC), I believe Intuit’s is able to access fresh capital at around 12% on average, peaking at around 15%. However, access to fresh capital is forward-looking (it is borrowed before it is deployed, based on assumed future returns), while the cost of capital is backward-looking (it assesses whether or not an equity investment in Intuit was better than an investment in the broader market, after the performance has been quantified). Therefore, the true cost of capital can only be determined in retrospect, and may not reflect the actual cost experienced by Intuit at any point in time.

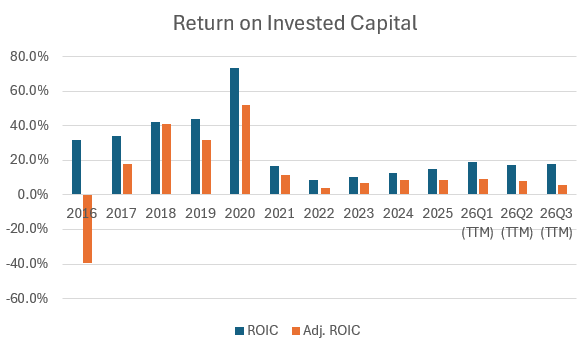

Return on Capital

Now that the cost of capital and level of debt has been established, it is time to look at the returns on that capital, and whether Intuit is able to generate returns above cost (and by how much).

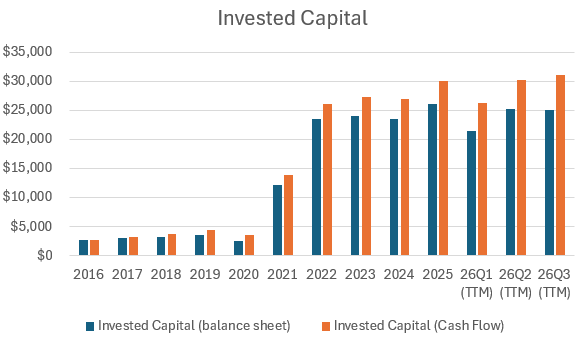

There are two ways of looking at invested capital: the first way is to use the current values of asssets and liabilities recorded on the balance sheet, but this will exclude the effects of depreciation and amortisation and ignore poor capital allocation decisions if investments have been previously impaired; the second way is to add back these expenses, so that all deployed capital is captured and the effect of impairments, depreciation or amortisation are captured. The second way is calculated by adding back the relevant non-cash operating expenses from the cash flow statements. This is the approach favoured by Michael Mauboussin.

Invested capital shows a rapid increase between 2020 and 2022, associated with the approximately $20 bn spent acquiring Mailchimp and Credit Karma. For calculating Return on Invested Capital (ROIC), I have also calculated two alternative metrics: I have used the textbook income statement and balance sheet values to produce a nominal ROIC value; and I have adjusted for the cash cost of SBC, as discussed previously, and the adjusted value of invested capital. This second approach is more aggressive, as the operating profit is reduced by the cash cost of SBC, and the invested capital is increased by excluding the effects of depreciation and amortisation. N.B. these are my own calculations and other sources may produce different values.

ROIC, as calculated by these methods, reveals two important traits. Firstly, the acquisitions appear to have been value-destructive. Acquisitions, conceptually, cause an increase in invested capital before those investments start yielding returns, so there is usually an initial drop in ROIC before it increases again. However, in this case, although ROIC has increased in the years following the acquisitions, returns have never been as high as before the acquisitions. Secondly, the effect of SBC is painfully obvious - ROIC has nominally been running at around 15% on average since 2021, but on an adjusted basis, ROIC has been closer to 7% - 8% on average over the same timeframe. The change in invested capital between the nominal and adjusted calculations is relatively small, so SBC is the primary driver of this difference.

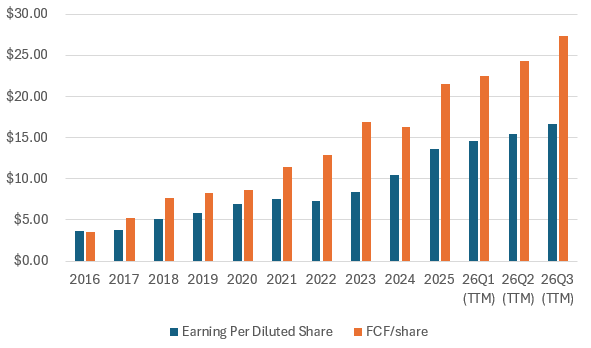

Earnings and Free Cash Flow

Although the acquisitions have lowered Intuit’s ROIC, another way to judge success is to look at the growth in earnings or free cash flow (FCF). Based on nominal earnings per share (EPS) or FCF per diluted share, Intuit has demonstrated consistently strong growth, with EPS growing at around 16% - 17% CAGR since 2016, and FCF growing at over 23% CAGR.

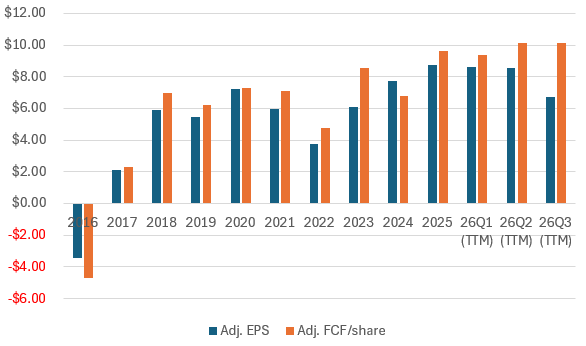

However, adjusting for SBC costs and excluding the period 2016 - 2017 shows growth has been much more gradual since around 2018, with EPS only returning around a 2% CAGR and FCF per share only growing at a 4% CAGR in that time.

FCF keeping pace with, or exceeding, earnings indicates that earnings quality is good, i.e. the declared accounting profits are backed by cash generation, even after considering the cash costs of SBC.

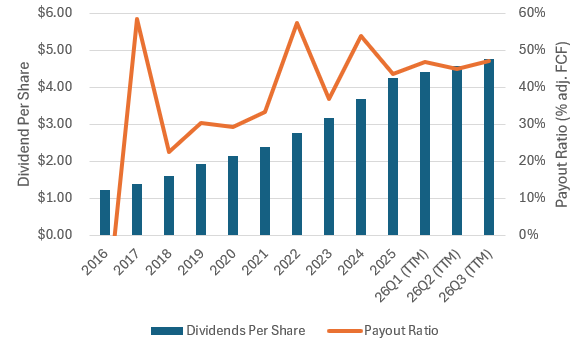

Dividends

Intuit pays a reasonable dividend, with strong dividend growth - dividend per share has been growing at 15% to 16% per annum pretty consistently since 2016. Dividend payout ratio has fluctuated over time, but has consistently been below 60% of adjusted free cash flow (i.e. FCF adjusted for the cash costs of SBC). This indicates that the dividend is sustainable and is growing at a similar pace to both earnings and free cash flow over the full period assessed.

Risks

Intuit call out a number of specific risks in their annual reports. Firstly, Intuit discuss competitive pressures, not least the fact that the IRS offers a free tax filing programme. Intuit’s revenue is primarily derived from North America (Intuit declared that only 8% of their net revenue is from international operations in 2023, 2024 and 2025), meaning they are specifically exposed to a loss of custom in the U.S. As tax is, in principle, a fully mechanistic process, there is an argument that it is particularly exposed to A.I. and automation. If this were to be realised to the fullest extent, this would expose Intuit, and its TurboTax product suite in particular, to material loss of revenue.

On the other hand, with such little international exposure, there could be ample opportunity for Intuit to expand abroad. When researching Sage, I saw that their management expected their Total Addressable Market (TAM) to grow at over 13% per year. Intuit is achieving growth at a higher rate than this, growing its Global Business Solutions segment at almost 19% CAGR, and growing its QuickBooks Online category at 17% last year and 31% CAGR since 2016. In Intuit’s 26Q3 earnings call, management imply TAM is around $42 bn for the TurboTax market, whereas Sage believe their TAM is between £39 bn and £50 bn. TurboTax delivers revenue of around $5 bn, or around 12% market share. QuickBooks provides revenue of close to $7 bn, or about 10% market share. This indicates Intuit has a strong market presence, but still has room to expand.

Intuit also recognises that its business is dependent on protecting their brands and intellectual property. Specifically, Intuit identify robust cyber security as a risk, given their need to host and access sensitive personal information and confidential corporate data for tax and financial purposes. The more of their custom that migrates to the Cloud environment, the more exposed Intuit could become to threat actors, particularly as actors of all types seek to exploit the capabilities of AI tools. In this context, one of Intuit’s strengths is also a weakness. By building a full ecosystem, enabling customers to have a single identity across multiple Intuit products, unauthorised access to one product or account could expose multiple sources of customer data.

With respect to AI, Intuit comment that uncertainty surrounding the development and deployment of AI tools could pose harm to their business, either due to the immaturity of tools or unexpectedly high development and validation costs, or from erosion of their business if 3rd-parties are able to develop more capable and advanced tools than Intuit.

Another particular risk Intuit have is their exposure to small business loans. Intuit provides a route to the capital markets for small and mid-sized businesses and, on occasion, purchases loans from 3rd-party lenders. This provides a source of interest income for Intuit, but exposes them to financial loss if borrowers default. Funds held for customers, which shows up as both an asset and a liability on Intuit’s balance sheet, accounts for up to 20% of total assets.

Another word on the risks and opportunities of AI

Intuit considers the development of AI to pose both an opportunity and a threat. The development of 3rd-party tools poses a risk to large parts of Intuit’s business if those tools can replace or improve upon the functionality Intuit currently offers at a lower cost. In their 26Q3 earnings call, Intuit identified a decline in DIY tax filers within their TurboTax segment. The narrative is that this provides evidence that users are starting to migrate to other tools, perhaps using native AI tools themselves to replace the TurboTax product entirely.

However, this is not the full story. Overall, TurboTax has been growing. Intuit saw strong growth in their TurboTax Live category, with high levels of new customer conquests, particularly where people wish to access a local tax expert. Intuit also saw increased revenue per user for customers using both TurboTax and Credit Karma, implying opportunity exists to leverage synergies by linking product offerings.

Last month, Charlie Huggins shared a research note from Panmure Liberum about AI. The note references research indicating that it may be impossible to stop Large Language Models from hallucinating, which would mean that these tools may not be fully able to replace offerings from companies like Intuit, where one of the major selling points is the trust, assurance and guarantees that Intuit can offer and generic AI tools currently can not. Panmure Liberum suggest the future of AI tool development for industries where legal or financial assurance are paramount may be exactly the type of Small Language Model AI agents Intuit are developing internally within their ecosystem.

Intuit accept that in the DIY-filer, lower-income, segment of the market, the TurboTax offering has not provided adequate value. Intuit will be focussing on the sub-$50,000 filers more intensely in the future to hone this value-sensitive product offering. Intuit is also shifting focus with its ProTax offering to accountants, to treat them more as customers in their own right, and less as a route to market for discounted product sales to end users.

This leads to Intuit’s TurboTax market bifurcating - in the less value-sensitive end of the market, where assurance is more important and customers consider the cost of the product to be relatively trivial, Intuit expects to be able to offer increased value from focussing more on their Accountant offerings and generating synergies across Intuit’s whole product suite. In the more value-focussed end of the market, where users are more willing to take assurance risk for a lower price point, Intuit’s customer base is more at risk from AI toolset developments and competitive pressures, and this will be an area of management attention in the coming years. In all cases, TurboTax’s guarantee to find and/or maximise eligible tax refunds and offsets for their customers is an important differentiator to generic AI tools, but this is a moat that could be eroded by further development of AI in such a rules-based framework as tax liabilities.

I believe a similar argument holds true for QuickBooks - I believe that, given the low nominal fee, few business owners would take the assurance and compliance risks, particularly with personnel records and bank accounts, etc., or give up on the integration offered by a bespoke product suite, or to expend the time themselves to develop AI prompts to an equivalent standard as that provided by Intuit. I also believe that for anyone with more complicated business arrangements, it is likely to be harder to robustly replace products like Intuit’s Enterprise Suite with individually-developed AI tools.

Valuation

For the nominal thesis, I have generated an estimate for intrinsic value using the following assumptions:

Revenue of $20 bn to $21 bn, growing at 13% to 17% per year

Earnings Before Interest, Taxes, Depreciation and Amortisation margins of 19% to 23% of revenue. This is the range where I calculate Intuit’s EBITDA margin to sit after adjusting for the cash cost of SBC

Depreciation and Amortisation costs of 13% to 18% of relevant assets

Capital Expenditure (including internal development) of 1% to 3% of revenue

An effective tax rate of 17% to 21%, representing the range seen since 2019 (excluding the two highest and two lowest annualised results since 2016)

Debt/Equity of 30% to 40%

A cost of debt of 3.6% to 3.8%

A risk-free rate of 4% to 4.5%, given current central bank rates, a market premium of 8% to 10% and a beta coefficient of 1 to 1.25, which provides a weighted cost of capital of 10% to 13%.

A dividend payout ratio of 50% to 60% (after cash costs of SBC)

Return on Capital of 6% to 9% and a terminal price multiple of 20 - 30

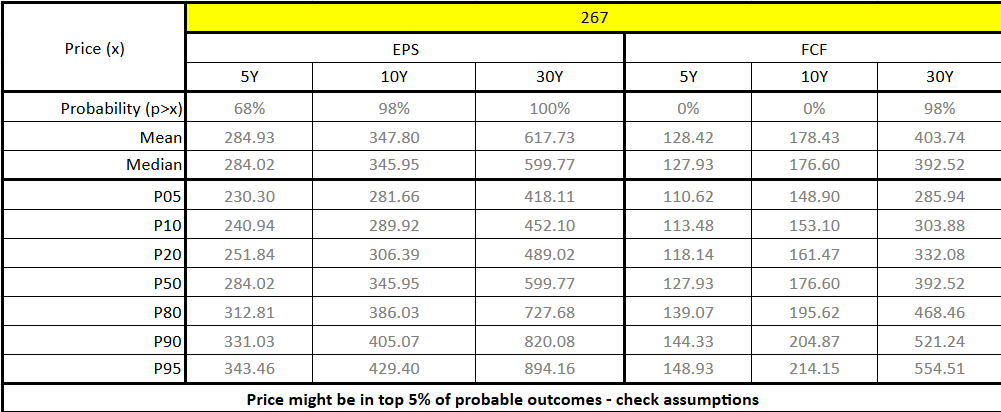

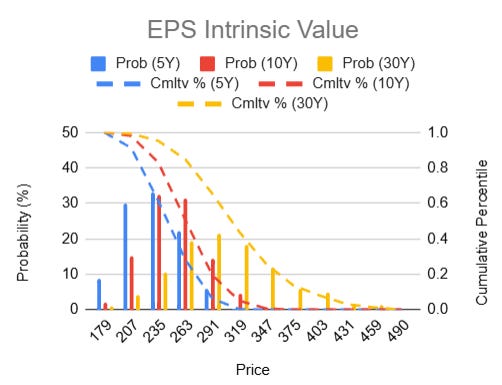

With such strong revenue growth, Intuit can justify a wide range of intrinsic values for different growth periods, even after allowances for the cash costs of SBC. On a 10-year discounted cash flow (DCF) basis, I believe these assumptions support an intrinsic value of around $300 per share, based on earnings after the cash costs of SBC. Longer time periods provide considerably higher intrinsic values, as revenue (and therefore profit) growth outstrips the cost of capital and present value discount factors. For transparency, my model also implies that fair value based on free cash flow after cash costs of SBC nearer to $200 for a 10-yr discounted cash flow, rising to $300 - $400 for a 30-year DCF analysis.

My modelled net present value for earnings and free cash flow results in estimates of around $10 per share for each metric, consistently, throughout the DCF period. However, the relative changes in depreciation cost and capital expenditure is such that a valuation based on FCF is more likely to generate slightly less than $10 per share in the near term, whereas a similar valuation based on EPS is more likely to generate slightly more than $10 per share in the near term. Over time, this compounds to a difference in fair value between EPS and FCF of $100 to $150 per share, exacerbated by the high revenue growth rate. This is because my modelled CapEx is based on a proportion of revenue, so high revenue leads to increased CapEx estimates. My modelled earnings per share is derived from operating margin and the capital base, incorporating depreciation costs but not CapEx costs. As I expect CapEx, including investment in internally-generated intangible assets, to be more easily adapted by management to the prevalent economic conditions than EPS, on this occasion I put more weight on the intrinsic value inferred by EPS than for FCF per share.

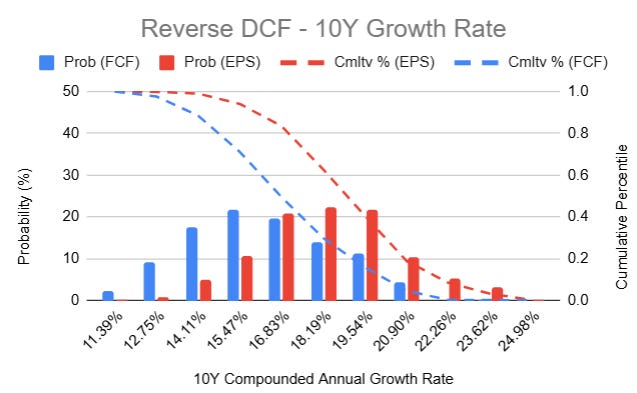

Reverse Valuations

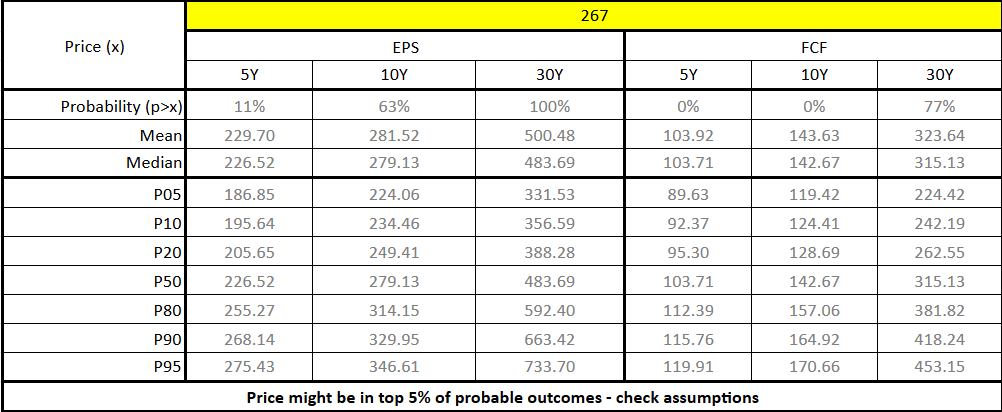

What would it take to justify the current share price of around $267?

All else being equal, I estimate that revenue growth of 11% - 12% would provide fair values in the range of the current share price.

… or EBITDA margins of 17% - 19% would do similarly, depending on the preferred metric and chosen timeframe.

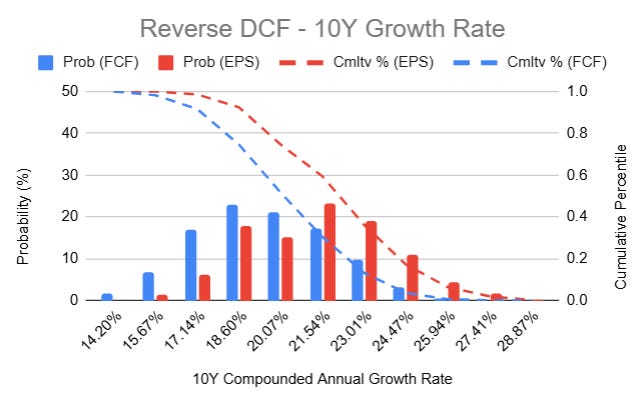

Currently, I calculate adjusted FCF/share to be slightly higher than EPS, even though my model expects this to reverse as revenue and CapEx grow. The current share price implies 18% to 24% annualised growth rate is required to provide intrinsic value, with a median growth rate requirement of 20% - 23%. This is slightly higher than has been achieved over the long-term, but is in line with what has been achieved in recent years.

Based on historical growth rates in EPS or FCF/share, after cash costs of SBC, the share price would have to drop to closer to $215 to provide intrinsic value.

On face value, this means that the current share price, at the current share count, could be justified even if revenue growth were to drop by approximately 3% - 6%, or if EBITDA margin were to drop by 2% - 4%. On the other hand, given the pressure being put on per-share earnings or free cash flow by SBC dilution, growth rates of up to 23% per year may be required to justify the current share price, or the share price would need to drop to around $215 to support the long-term growth rates presently being demonstrated.

The Bear Case

What if the AI fears are correct, especially around TurboTax, leading to a maximum loss of $5 bn of revenue per year? If all TurboTax revenue and operating profit were to be lost, but unallocated corporate expenses were to remain unchanged, I would anticipate operating profit margin dropping from around 26% (nominally) to around 8%. In this case, the intrinsic value could be as low as $40. If operating expenses could be managed, such that operating profit margin remained in the 19% to 23% range even without TurboTax revenue, an intrinsic value of $160 - $180 might be justifiable.

Conclusions

With a current share price of around $267, Intuit is around my estimate of intrinsic value, based on its current business and on the assumption that the business continues to be similarly strong in the future as it is today.

If the prince were to drop to nearer $200, I think Intuit would offer very good value by almost any measure.

I think the biggest short-term risk is not from AI, but from the cash impact of stock-based compensation, which considerably depresses my estimates for free cash flow and earnings. Although I don’t like the peer group selection, I do like Intuit’s choice of metrics for assessing corporate performance for equity awards in both the short and long term. Despite this, I think the return on capital has been aggressively depressed by the combination of the Mailchimp and Credit Karma acquisitions and SBC. However, if you think this risk is overblown, I believe today’s price is attractive for the current level of business performance.

If you think AI does pose an existential threat to elements of Intuit’s business, such as TurboTax, then you may not be willing to invest unless Intuit dropped a further 60% from today’s value, despite Intuit having dropped 65% in the last twelve months.

Personally, at below $300, I believe Intuit warrants a small position in my portfolio. Although I think this is still expensive, and may require an investment horizon of over a decade to provide a reasonable return, I believe Intuit offers enough value to weather the uncertainty of the current AI environment. I have recently added Intuit to my portfolio.

A link to my previous Sage research: