Investing Strategy: Dividend Investing vs Growth Investing

Investing Strategy: Dividend Investing vs Growth Investing

A theoretical example using ROIC to compare a dividend investing strategy to a growth comoany

I first published this in December 2023 on the Trading 212 app in the Dividends community, under the username “Anathema”.

A recent discussion with [Trading 212 users] Patrick and Pauley got me thinking about the age-old growth vs dividend investing. I thought I'd create a theoretical example.

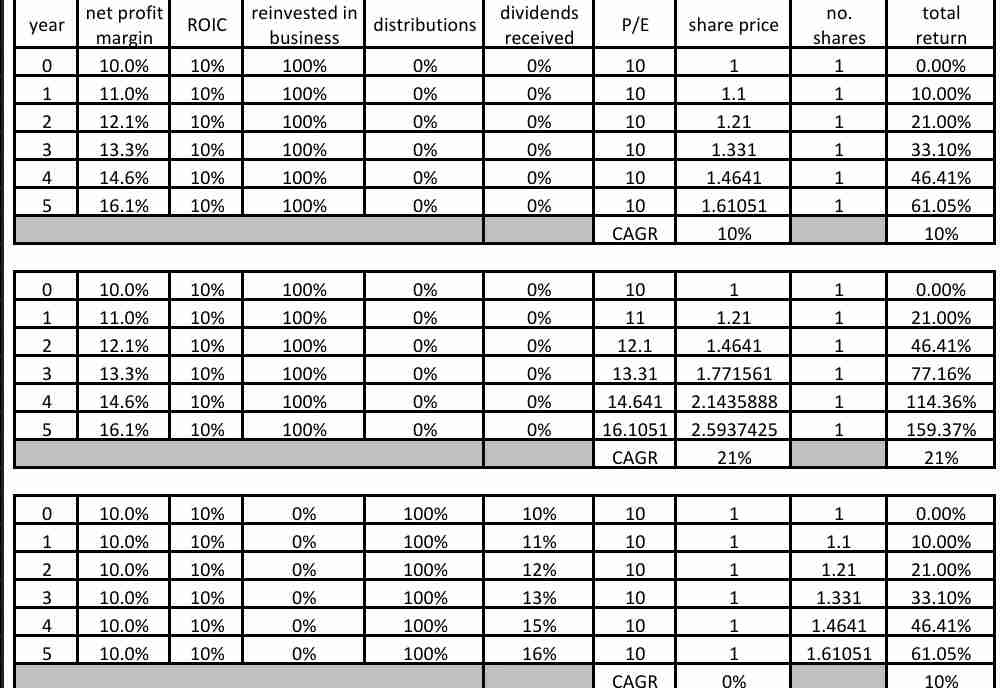

Let's assume there is a company which achieves a 10% net profit margin (or free cash flow). And let's assume this company also achieves a 10% return on its invested capital. And further, let's assume this company has a P/E of 10, giving it a PEG ratio of 1.

Every year, this company has 10% of its revenue to either reinvest in the company or to re-distribute to its shareholders. In the extreme, it can either entirely reinvest this money or entirely distribute it to shareholders.

If the money is reinvested, you would expect it to then enable the company to earn higher profits in the future, because that 10% profit would then increase by 10% each year via ROIC, meaning profit margin next year would be 11%, then 12.1% the following year, etc.

If you owned a single share of this company, after 5 years its profit margin would have increased from 10% to 16.1% and, if its P/E remained at 10, its share price would have increased by 61% (equivalent to 10% per year CAGR).

But higher profit margins and better growth prospects tend to command higher multiples. If, instead of P/E remaining at 10, PEG remained at 1, then after 5y, P/E would have increased to 16.1, and the share price would have increased by 159% from its starting value - a CAGR after 5y of 21%.

Conversely, if, instead of reinvesting the profits, the company distributed them entirely to shareholders, then each year the company would make 10% profit. If the revenue didn't increase, neither would profits. There would be no compounding via ROIC and, 5y later, earnings would still be 10% and P/E would still be 10.

If the shareholder reinvested the dividends, the shareholder would be able to buy extra shares with their dividend income. As each share carries its own dividend, every year the total amount received via dividends would increase because the shareholder owned more shares than the prior year, providing the same level of compounding as ROIC did in the growth example. After 5y, the shareholder would own 1.61 shares, a CAGR in share ownership of 10%.

In both cases, because all of the profit ends up in shares, it all remains fully exposed to the same investment risk.

So, when choosing between growth or dividend investments, the real question to ask yourself is ... do you think the P/E multiple can expand from its current value?

If you think, instead, the P/E is more at risk of a contraction, how much of your investment do you think is at risk (or do you think you can earn a return faster than the multiple can contract)?

I've created a small scenario example in the attached graphic to demonstrate.

Let me know if you find this helpful, or if you think I've misrepresented anything - I realise this might be quite obvious to some people, but I find it helps me to work through the details of some of these concepts, so I assume it might be helpful to some others, too.