Premium Bonds

Are National Savings & Investments' Premium Bonds a good investment?

Spoiler alert: the answer is going to be “if you think so”. But after a debate on the Trading 212 app about the pros and cons of Premium Bonds, I accepted the challenge to dive a little deeper into the odds of winning

Who are NS&I?

National Savings and Investments (NS&I) is a state-owned savings bank in the UK. One of its best-known products is Premium Bonds. NS&I is a “financial institution” (but not a traditional bank), which began life in 1861 as the Post Office Savings Bank. Being state-owned, and therefore part of the government, it is backed by HM Treasury and 100% guarantees savers’ money. Unlike a traditional bank, it does not lend money to individuals or businesses - money deposited by savers is being loaned to the government.

What are Premium Bonds?

Established 30 years ago in 1994, Premium Bonds are described as a cross between a lottery and a savings account, run by NS&I. Each bond has a face value of £1, and an eligible individual can hold up to £50,000 in Premium Bonds. Unlike a savings account, the bonds do not pay interest, instead being entered into a prize draw each month. And unlike a lottery, the creditor’s capital is guaranteed, meaning the creditor will not lose money, even if they don’t win anything.

This means that, although the creditor won’t lose money, the creditor could lose spending power, as that capital is eroded by inflation over time, unless the winnings from the prize draws matches or exceeds the cost of inflation.

How does the prize draw work?

NS&I set a likelihood of any bond winning a prize. They can arbitrarily change this prize rate, and by doing so, they effectively dictate the expected value of winnings for any bond. Currently, the likelihood of any bond winning in the draw is 1 in 21,000 but the likelihood of winning is dropping to 1 in 22,000 from December 2024.

There is a prize fund, divided up into different numbers and values of prizes. The prize fund is divided into Higher Value, Medium Value and Lower Value bands, with proportions of the total fund allocated to each band. The division is (roughly) as follows (there is often some rounding required as the band is broken down):

Each month, there are two £1,000,000 jackpots

Half of the Higher Value band’s fund is allocated to £100,000 prizes, giving a certain number of prizes

Half of the remaining Higher Value band’s fund is then allocated to £50,000 prizes

Half of the remaining Higher Value band’s fund is then allocated to £25,000 prizes, then again to £10,000 and finally to £5,000 prizes

This means there are approximately twice as many prizes when the prize value is halved from the previous amount.

The Medium Value band’s fund is divided between £1,000 and £500 prizes, such that there are 3 prizes of £500 for every prize of £1,000.

The Lower Value band’s fund is divided such that there are an even number of £100 and £50 prizes, with the remaining fund being used for £25 (respecting the number of eligible bonds and the overall likelihood of winning).

All prizes are tax-free.

Example Prize Breakdown

In September 2024, the Higher Value band accounted for 10% of the prize fund, as did the Medium Value fund, meaning 80% of prizes were of £100, £50 or £25. The full breakdown was:

2 prizes of £1,000,000

88 prizes of £100,000

175 prizes of £50,000

352 prizes of £25,000

877 prizes of £10,000

1,757 prizes of £5,000

18,361 prizes of £1,000

55,083 prizes of £500

over 2.2 million prizes each of £100 and £50

almost 1.5 million prizes of £25

Overall, there were 5.96 million prizes given out, with a total prize fund value of £459 million. To scale the amount of money held in Premium Bonds, at a likelihood of winning of 1 in 21,000, this many prizes implies that over £125 billion was held in Premium Bonds in September. If everyone held a full £50,000 allocation (and obviously many people will not hold this amount), that would still mean 2.5 million people held Premium Bonds. In fact, over 21 million people, or roughly 1 in 3 people in the UK, hold some amount of Premium Bonds (including me).

The prize fund and odds of winning are set so the prize fund provides estimated (but not guaranteed) ‘average’ returns of 4.4% on invested funds currently (dropping to 4.15% in December 2024).

Are Premium Bonds worth it?

So if you hold Premium Bonds, how likely are you to win and how much are you likely to win? Obviously, ‘it depends’ - as it is random. So I built a bit of a model to try and dig in a little.

TL;DR - if you want to cut to the chase, have a look at this article by Martin Lewis on MoneySavingExpert - he says the same thing but in fewer words!

But for those who want the detail, keep reading!

The Model

I set up a 50,000-line Excel spreadsheet to assess the likelihood of winning, with each line representing an individual bond. I used the RAND() function to pick a number between 0 and 1, and if the number was less than 0.0048% (1 in 21,000), I designated the bond a ‘winner’, otherwise it was a ‘loser’.

Using the September numbers, I discretised the prize fund into likelihoods of winning between 0 and 1. For example, 2 of the 5.9 million prizes were £1M, so if the random number generated a number between 0 and 3.36 x 10^(-7), it won the £1M prize; if the random number was between 3.36 x 10^(-7) and 1.51 x 10^(-5), it won £100,000; and so on down through the prizes until reaching a number between 0.75 and 1, representing a £25 prize.

Once a bond was a designated ‘winner’, I used another random number to select which of the prizes that bond would win, based on the above thresholds. This (whether a bond was a winner or a loser and what prize is would win if a winner) represents a single month’s draw.

I then summed the results for different numbers of bonds to represent different sizes of holdings.

I repeated this exercise 24 times to represent 2 years of Premium Bond holdings (it’s not quite comparable, but Central Limit Theory suggests a sample size of 30 is often reasonable to reveal distributions, so I was concerned that one year of draws (a sample size of 12) may not be sufficient to get consistent results, especially for the smaller holdings). I then undertook a couple of different analyses:

I summed the winnings over different holding sizes and divided by 2 to get an average annual winnings for each holding

I calculated the average rate of returns by dividing that average annual winnings by the size of holding

I summed the winnings over only the first 12 samples to represent a single year’s draws, just to provide some idea of variability

Using the full 24 draws, I found the median monthly winnings and multiplied by 12 for an equivalent annual rate.

The results are shown below:

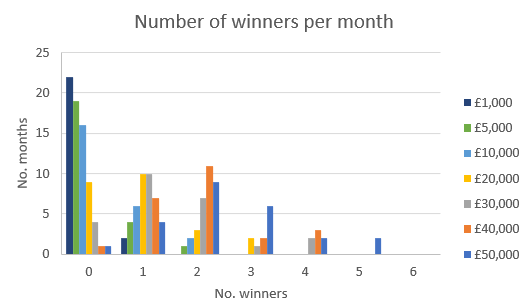

For smaller holdings (£10,000 or below), the majority of draws resulted in no winnings (Figure 1)

At £20,000 and above, it was more likely than not that at least one bond would win

With a full £50,000 allocation, the average number of winning bonds per month was 2.36 i.e. between 2 and 3 bonds would typically win a prize each month

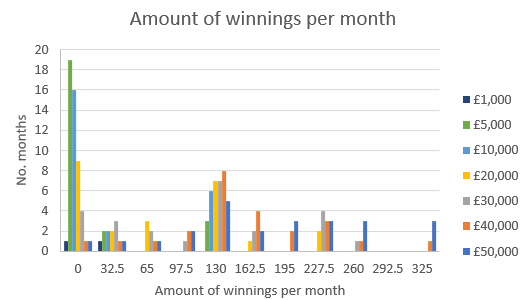

With only £1,000 holding, it was often the case that no bonds won at all. When a bond did win, it was a low value prize (either £25 or £50). See Figure 2.

With a holding of £5,000, there was at least one winner most months, but monthly winning were usually £25 (although there were 3 examples of winning between £100 and £125 in a single month)

With larger holdings, monthly winnings became more distributed, with the highest winnings in a month being £325, but the most frequent amount to win each month was between £100 and £125

the rate of return for low holdings sizes was more variable between the 1-year and 2-year sample sizes (Figure 3)

At £20,000 investments or above, the rate of return tended to around 4%, slightly lower than the nominal rate of 4.4%

The effective rate based on median winnings was zero up to around £10,000, only reaching the ‘average’ rate with a holding of £30,000 or so

So are Premium Bonds Worth It?

My quick study suggests that, on average, you will likely get a rate of return close to the target rate with most sizes of holdings, but this rate will be highly variable with less than £20,000 - £30,000 invested. However, with a holding of less than £20,000, most of the draws will result in no winnings at all.

However, for me, Premium Bonds are a good way to achieve reasonable rates of return with the opportunity to win much more, so long as there is a sizeable holding.

I would be happy to hold £20,000 or more in Premium Bonds as my emergency cash fund. How about you?