Quick Dip: Anglo Teck

In contrast to my regular deep dives, I want to take a quick glance at the Anglo Teck merger and decide if Anglo American still looks like good value, given its recent run-up

Almost 2 years ago, in the aftermath of BHP’s aborted takeover bid, I dissected Anglo American’s (LON:AAL) assets to try and determine whether the BHP bid looked like fair value or not.

At the time, I felt that the value of AAL’s assets were greater than BHP were willing to pay, and AAL could achieve higher values than the approximately £31/share inferred by BHP’s offer.

With Anglo American’s shares trading at over £38 at the time of writing, it seems the board were right to reject the bid! But with the merger with Teck Resources now on the cards, does £38 per share represent good value for the future company, or is now a good time to realise some profit?

Disclaimer: This article is intended for information only and should not be used as the basis for any investment. I am not a financial advisor and nothing I say should be considered financial advice or a recommendation to buy or sell. Opinions expressed are my own and, although I have made best efforts to ensure the accuracy of any data expressed, I cannot guarantee this article is free of error. At the time of writing, I hold shares in Anglo American.

The BHP Aftermath

Valterra

Following BHP’s takeover attempt, AAL spun out its Platinum Group Metals into Valterra (LON:VALT) and then divested its holding. As shown in my previous deep dive, both BHP and I had estimated the value of AAL’s platinum business at around £5/share (I believed AngloPlat was worth £5.18/share, BHP had quoted £5.40/share). AAL demerged 51% of its interest (so around £2.50 - £2.75 per AAL share) and, in order to manage the share price (which would otherwise have dropped correspondingly), AAL consolidated its shares at the same time to reduce its issued share capital by around 12%1.

This means that my previous intrinsic value of “over” £31/share (i.e. more than BHP were prepared to pay) remained valid, as the intrinsic value was reduced by an approximately similar amount to the reduction in share capital issued.

Valterra listed at around £23 per share, and is currently trading at around £65 per share, having peaked at over £86 per share. This seems to have been a positive unlocking of value for shareholders.

Steelmaking Coal

AAL were in the process of selling their Australian steelmaking coal business to Peabody Energy Corporation, when they experienced a fire in their Moranbah North mine, within their Grosvenor business unit. Peabody pulled out of the deal, stating the fire constituted a Material Adverse Change, which AAL dispute2. Having re-listed the asset for sale, Anglo American are now reported to have 3 bidders for their steelmaking coal assets3.

The Peabody deal was going to be worth $3.8 bn, or close to £2.8 bn, which is a little over £2/share, based on AAL’s current share count. Whether or not this value can still be realised with the new bidders and the current state of the mining assets remains to be seen.

De Beers Diamonds

Following several impairments and write-downs, De Beers is now valued at $2.3 bn, or £1.7 bn at current exchange rates4. On the current share count, this is equivalent to around £1.43/share. Anglo American is currently actively looking to sell its 85% stake in the company.

Residual Assets

Excluding coal, platinum group metals and diamonds, Anglo American is left as a predominantly copper and iron ore miner, with some minor interests in manganese and crop nutrients (currently being slow-rolled while seeking investment partners). From the valuations I had developed as part of my previous sum-of-the-parts valuation, I had previously estimated that these assets would have been worth something like £35/share. Considering the held-for-sale coal and diamond assets, this implies an AAL share price of around £38/share, roughly where it is trading now5. One view is that the current share price therefore still represents fair value for the current AAL assets.

Teck Resources

Teck is a copper and zinc miner, headquartered in Canada. Importantly, some of Teck’s copper assets are in very close physical proximity to Anglo American’s existing copper assets in Chile, and the ability to realise synergies from combining operations is a strong part of the rationale for the proposed merger. Specifically, Teck’s Quebrada Blanca asset is adjacent to Anglo American’s Collahuasi asset, which is itself a joint venture where AAL hold a 44% interest.

The Terms of the Merger

Fundamentally, the proposed deal is classed as a Merger of Equals, however, in practice, Anglo American will issue 1.3301 shares for each common share of Teck6, with the intent that existing Anglo American shareholders then own 62.4% of the combined company.

Anglo American also intend to issue a special dividend of US$4.19 per share ahead of the merger, US$4.5 bn in total.

With almost 490M diluted Teck shares in issue, this implies issuance of another 650M Anglo American shares (the merger is actually requesting an extra 664M shares), which is around a 60% increase in shares issued. This will therefore look like significant dilution to Anglo American shareholders, although they will receive the value of Teck’s assets (and liabilities) in return.

So the big question is - will AAL shares be worth more as Anglo Teck, or is the current value of AAL likely to indicate a significant premium, compared to what is on offer via Anglo Teck?

The Synergies

Anglo American’s circular to shareholders to explain the merger proposal lays out the following opportunities:

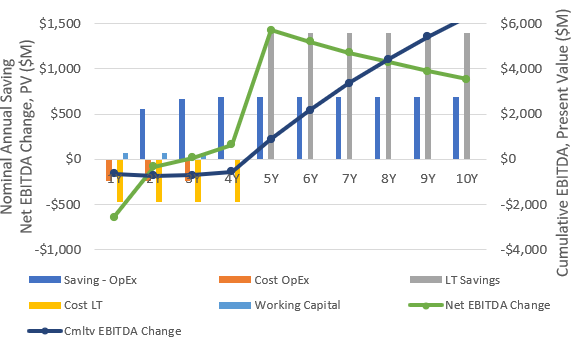

US$800M annual pre-tax synergies within 4 years of the merger, with 80% of these savings being achieved by the end of the second year following the merger, and US$775M achieved within 3 years of the merger. Sources of savings are economies of scale, operational efficiencies, and “commercial and functional excellence” (whatever that means). In essence, there should be a reduction in operating expenses, relative to the combined costs of the two individual operations, split across cost of goods sold and selling, general and administrative costs. However, the board expects to need to spend US$700M in cash over the first 3 years after the merger to realise these benefits. The breakdown of the savings is:

US$60M savings from consolidating board and head office costs

US$150M savings from reduction in corporate overheads by removing duplication and aligning overlapping functions

US$490M savings from direct and indirect procurement, of which around US$110M is expected to be from synergies in Capital Expenditures (CapEx)

US$100M savings from marketing revenue by leveraging best practices across both operations

US$1.4 bn per year, on average, in additional earnings before interest, taxes, depreciation and amortisation (EBITDA) between 2030 and 2049 by integrating Quebrada Blanca and Collahuasi operations. However, this is expected to require capital investment of US$1.9 bn in total, spread across the first 4 years after merger.

Unquantified further revenue growth opportunities, with an increase in potential annual production capacity of 175 ktonnes, following realisation of the above synergies.

A one-off US$200M in cash savings from improved working capital management (inventories and payables), to be realised within 3 years of the merger. No material cash outlay is expected to achieve these savings.

Show Me The Value

Underlying EBITDA

Anglo American’s 2025 Underlying EBITDA was US$6.4 bn, or around $5.67 per share, compared to $5.22 per share in 2024. Teck’s 2025 Adjusted EBITDA was CAD$4.3 bn, or about US$6.25 per share, compared to US$4.12 per share in 2024 (Teck quote effective USD/CAD exchange rates at 1.40 in 2025 and 1.37 in 2024).

Had Anglo American and Teck already merged at 1.3301 AAL shares for each Teck share, the combined Anglo Teck company’s underlying EBITDA per share would have been US$5.31 per share in 2025 and $4.45 per share in 2024. These numbers are less than Anglo American’s individual underlying EBITDA per share, indicating that this merger may not offset the dilution without realising the targeted synergies.

If a cost of capital is assumed at around 10% (I have previously estimated AAL’s cost of capital at between 8% and 10%7), a present value for the future Anglo Teck after synergies can be estimated. Based on the information in their shareholder circular for the merger, I will assume:

80% of the Operational Expense savings are achieved in Year 2, $775M (less $110M for CapEx) are achieved in Year 3, and $690M (the full $800M less $110M CapEx) are achieved in Year 4 and recur thereafter

Costs of $233M are incurred for each of the first three years to support those OpEx savings, dropping to zero cost from Year 4

The long-term savings do not occur until Year 5, then recur at $1.4 bn each year from Year 5 onwards

The business incurs $475M each year for the first 4 years ($1.9 bn in total) to support the long-term savings of $1.4 bn per annum, with costs dropping to zero from Year 5

$66.7M of working capital savings occur in each of the first 3 years following the merger, then drop to zero from Year 4 onwards

The net annual EBITDA effect at present value turns positive by Year 3, and peaks in Year 5 (the discount factor reducing the present value thereafter). Cumulatively, underlying EBITDA should become positive in Year 5, and could be worth over $6 bn in total, at present value, by ten years after the merger.

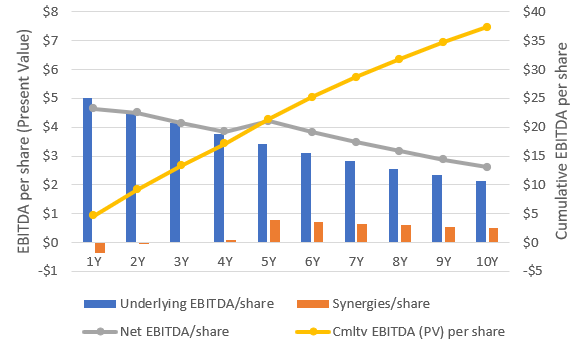

If EBITDA for the combined company continues to generate around $5 per share (a very naive assumption with scant consideration of commodity prices, this is just to provide an example), still with a 10% cost of capital, the underlying EBITDA on a discounted cash flow basis could be worth $37 per share (or around £27/share at an exchange rate of US$1.36 to each GBP). This is about 70% of the current share price, but interest expense and taxes will mean that the intrinsic value available to shareholders will be lower than this, and therefore more of the current share price is being ascribed to earnings further into the future, or the terminal value of the stock.

Below, I will attempt to separate the company into the copper company and all others.

Copper Assets

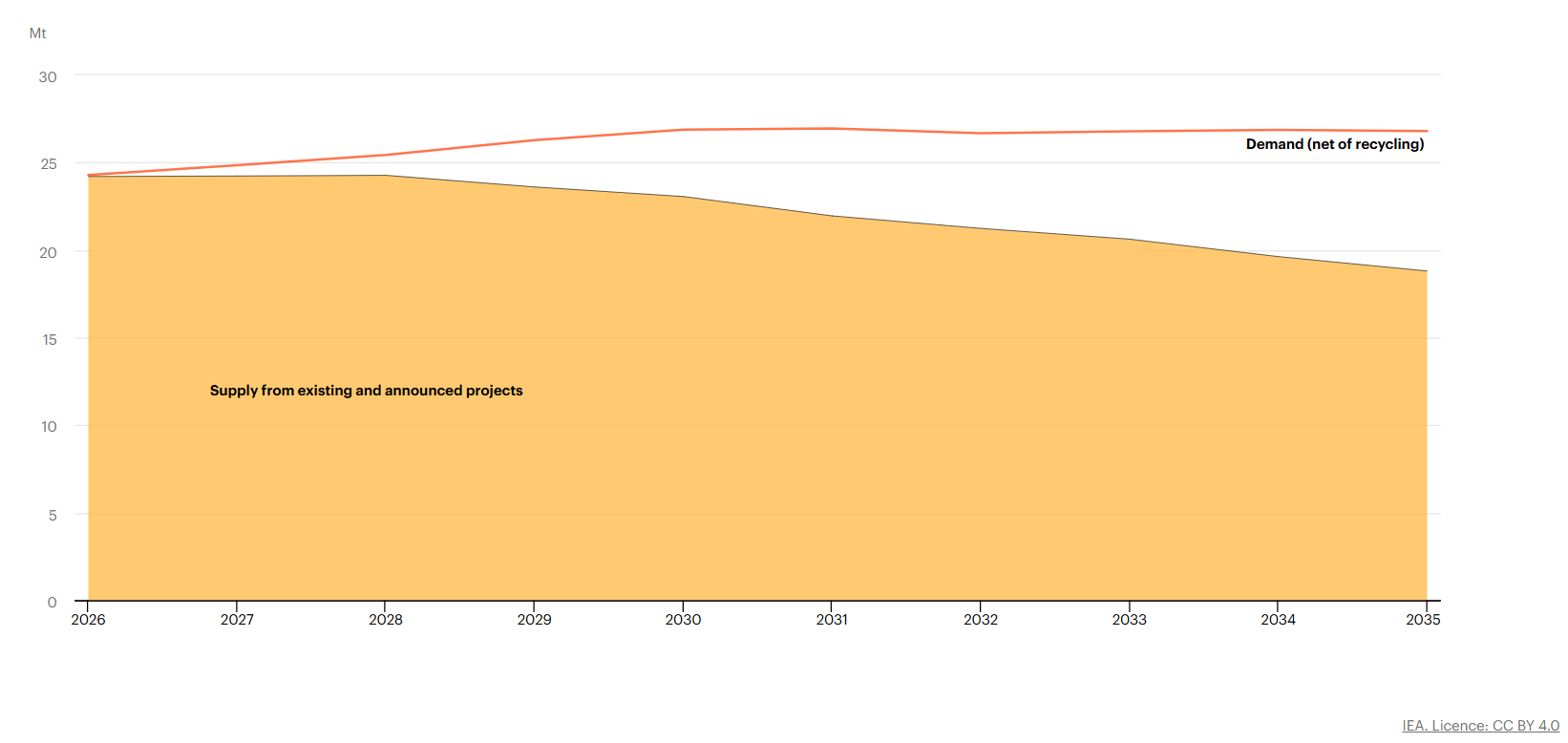

According to the IEA, copper supply is expected to be a little under 25 Mtonnes in 2026, dropping to less than 20 Mtonnes by 2035, while demand is due to increase to 26 - 27 Mtonnes over the same timeframe8. This means the IEA is anticipating the copper market to move from around parity today, to a production deficit of around 30% by 2035. The IEA also makes explicit reference to the availability of smelting facilities, and the fact that a large amount of smelter capacity is located in China, i.e. there is a high geographic concentration risk.

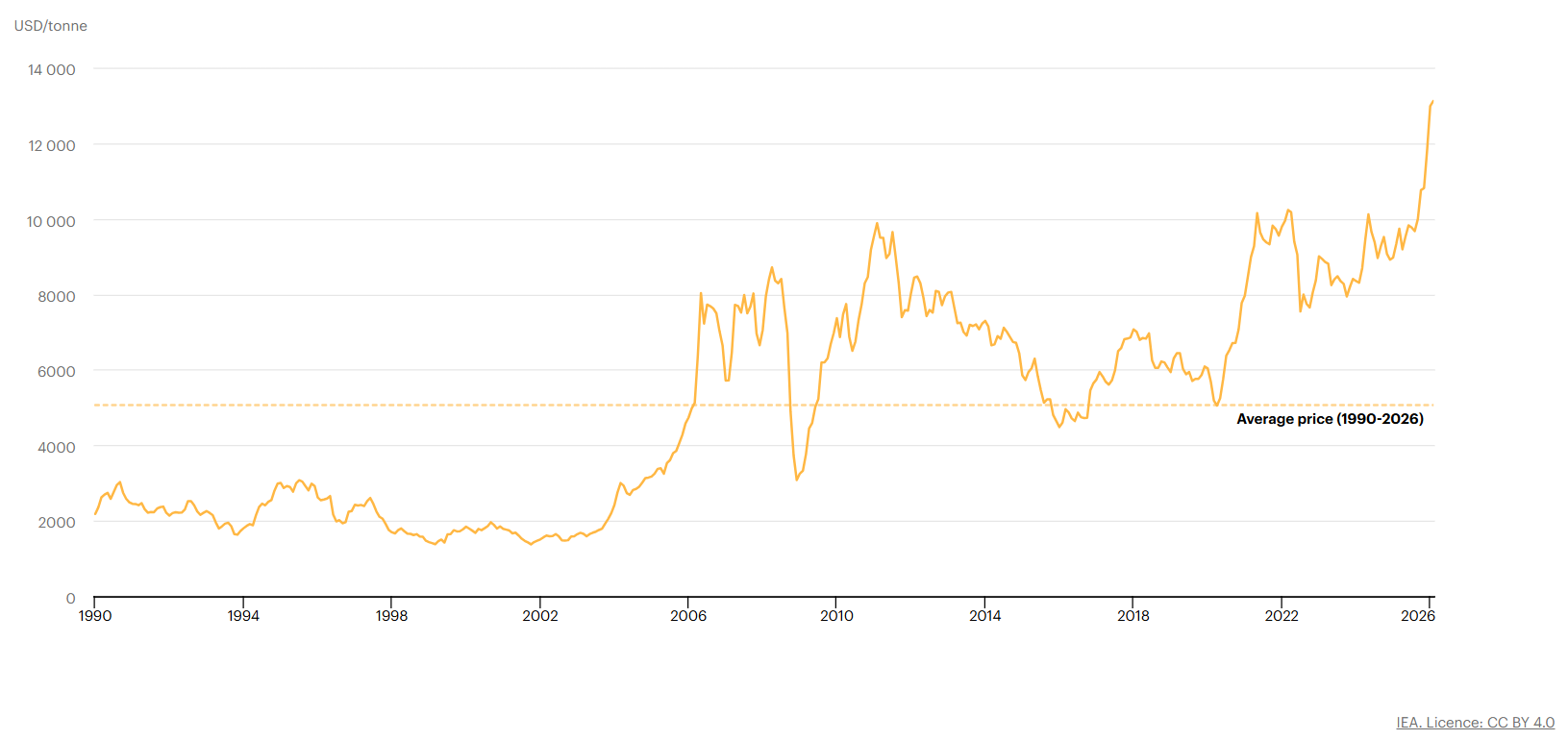

In 2025, AAL produced 695 ktonnes of copper across its Chile and Peru operations (although they had produced 772 ktonnes in 2024), and Teck produced 454 ktonnes, with a similar amount (446 ktonnes) produced in 2024. Even as a combined entity, they are relatively small on a global scale, accounting for a little under 5% of global supply. However, as commodity suppliers, AAL and Teck both stand to benefit from the recent rise in copper prices. Copper is often quoted in USD/lb, so to contextualise the figure below, it is helpful to know that $5,000 per tonne is equivalent to $2.27/lb and $13,000 per tonne is equivalent to $5.91/lb. Copper is currently trading above $6/lb in the futures market.

If the IEA report is relatively accurate, and supply will continue to tighten relative to demand, indicating that commodity prices will continue to rise, it is reasonable to assume that revenues will rise in 2026 by 20% - 30% (assuming an average realised price of over $6/lb, vs. something closer to $5/lb in 2025).

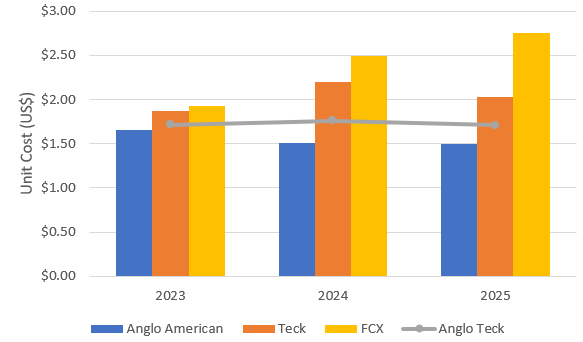

Looking at the unit costs quoted by Anglo American and Teck for their relevant businesses (weighted by production volume where the information is available), it is apparent that Anglo American has a lower unit cost base than Teck, but even as a combined entity, it remains competitive against some of its peers (I’ve used Freeport McMoran (FCX 0.00%↑) as a reference, as it is the other copper producer in my portfolio, but also because its Grasberg operation in Indonesia was one of the lower-cost production assets when I reviewed a number of holdings in 2024; the key alternative low-cost assets were the BHP/Glencore Escondida asset and Glencore’s Antamina asset9, which had a unit cost similar to FCX’s Grasberg asset)

Intrinsic Value of Copper Assets

Trying to generate a rough estimate of fair value for the Anglo Teck copper assets, I’ve made some very, very crude assumptions:

Production volumes continue at 2025 levels until 2030, when Anglo Teck realises its targeted 175 ktonne additional copper production. This means annual production of 1,149 ktonnes until 2030 and 1,324 ktonnes thereafter

Copper retains a market price of $6/lb

Anglo Teck’s unit costs of production are $2.20/lb, increasing by around 3% per year. This is highly dependent on the value of by-products and ore grade, etc. This number could vary widely, but is in line with 2026 guidance from the companies and historical performance.

Depreciation, Depletion and Amortisation (DDA) expenses of $1.1 bn per year, increasing each year by 2% of the previous year’s CapEx (implying a 50-year mine life, which is approximately the weighted average mine life of the Anglo American copper portfolio)

CapEx of 1.3 times that year’s DDA expenses (close to recent average CapEx-to-DDA ratios for the combined AngloTeck company). This means CapEx starts at $1.4 bn per year, rising to $1.8 bn by 2035.

All other operational costs of around $2.4 bn, increasing by 3% each year. This would generate a roughly 40% EBIT margin initially, which I believe is reasonable given recent performance and as estimated for the combined group following underlying EBITDA gains. EBIT margin would then decrease as copper price is assumed to be flat but costs and DDA continued to ramp up. The average EBIT margin over the next 10 years would come out at around 33%.

Free Cash Flow is estimated as EBITDA less CapEx, based on the above assumptions

A 10% discount factor to reflect a 10% cost of capital

1,790M diluted shares outstanding (reflecting the 1,131M current Anglo American shares and the 495M Teck shares, at 1.33 Anglo American shares for each Teck share)

Given the above, based on a 10-year discounted cash flow (DCF) assessment, I would expect Anglo Teck’s copper assets to be worth around $20 per share, or around £15/share. If a terminal growth rate of 3% is assumed, a terminal value might be $14 or £10 per share, giving an estimated intrinsic Anglo Teck value of around £25 per share. Adjusting this back to the current Anglo American share count of 1,131 shares outstanding would indicate an intrinsic Anglo American share price of around £39 per share, i.e. similar to the current price.

To provide some idea of sensitivity, with all of the same assumptions but permitting the market price of copper to shift from $4.50/lb (closer to 2025 average realised price) to $7/lb (which would be unprecedented), I would estimate the following intrinsic values for Anglo Teck:

At $4.50/lb copper market price → Anglo Teck intrinsic value of ~£17/share

At $5.00/lb copper market price → Anglo Teck intrinsic value of ~£20/share

At $5.50/lb copper market price → Anglo Teck intrinsic value of ~£23/share

At $6.00/lb copper market price → Anglo Teck intrinsic value of ~£25/share

At $6.50/lb copper market price → Anglo Teck intrinsic value of ~£28/share

At $7.00/lb copper market price → Anglo Teck intrinsic value of ~£30/share

This indicates an increase in intrinsic value of £5 per share for every $1/lb increase in copper price.

Other Assets

Based on Underlying EBIT, Anglo American’s copper business alone constituted 56% of their combined copper and iron ore and manganese businesses (it’s more like 70% of the group EBIT, considering the losses currently being experienced from De Beers, Woodsmith crop nutrients and corporate overheads). Combined, iron ore and manganese contributed around $2.2 bn to underlying EBIT in 2025.

Corporate overheads cost the business $545M, and, with $1.3 bn of interest expenses (closer to $0.9 bn net expense after interest income and capitalisation), interest cover was around 3 time underlying EBIT. The effective tax rate, on an underlying basis, was around 52% in 2025 and 46% in 2024.

Teck’s Zinc business generated operating profit of around CAD$821M (US$586M) in 2025, 36% of group operating profit. Teck had corporate expenses of CAD$715M (US$510M), with interest cover of around 2.5 times, based on operating profit (after capitalised borrowing costs), and an effective tax rate was around 35%.

Bundling these aspects together, an approximate contribution to the group of US$400M - US$500M could be assumed after corporate expenses, finance interest and taxes. Against a share count of 1,790M shares outstanding, this is only worth around $0.25 per share (or £0.18 per share).

In other words, grouping all other operations with all corporate costs, interest expenses and tax expenses, the net contribution to the bottom line is close to zero. Or, put another way, the valuations based on copper assets happens to be approximately similar to the overall corporate performance (based on 2025 performance and prices).

Cash and Debt

Anglo American is relatively highly levered, with debt/EBIT somewhere around 3 times and net debt to EBIT of around 2 times. In contrast, Teck currently runs a net cash position. After combining the businesses, considering the contribution of $2.2 bn from Anglo American’s non-copper businesses and Teck’s Zinc business, I estimate debt/EBIT may drop to closer to 1.5 times, with net debt of around $9 bn. This is a similar level of net debt to Anglo American’s current position, but against a larger company with stronger earnings.

Conclusion - is Anglo American still good value?

I believe it is. I think the current share price represents a reasonable value for the future combined Anglo Teck company, especially if Anglo American can offload its De Beers and coal assets at something close to book value and therefore stem current losses in these business units. Although I haven’t run a full valuation or looked at how returns on capital might be affected after the merger, I believe the combination of Teck’s more conservative balance sheet, the expected capital return to shareholders on completion of the merger, and the possibility that copper prices could continue to experience upward pressure in the medium term, means that this could still prove to be a good investment, even after accounting for the dilution required to buy out Teck’s existing shareholders.

However, there are risks that I have not assessed here - for example, I have not looked at either company’s debt maturity profile, and Anglo American quite often has considerable levels of exceptional items, causing statutory profits to vary significantly from the underlying profits I have used in this article. There is also a risk that Anglo Teck will not realise the synergies they are expecting, or that commodity prices may drop in the future.

This is not intended to be a comprehensive analysis, only a quick assessment of whether there is an obvious dislocation between current price and likely future performance. My conclusion is that the current price seems reasonable, and I will continue to hold Anglo American shares for now.

https://www.angloamerican.com/media/press-releases/2025/02-06-2025

https://www.angloamerican.com/media/press-releases/2025/19-08-2025

https://www.mining.com/anglo-american-draws-three-bidders-for-coal-sale/

https://www.ft.com/content/13357dd7-ffb3-4c1e-b2b3-4b6985e8fc1d?syn-25a6b1a6=1

Technically, De Beers is not yet held for sale, and I have excluded AAL’s nickel business, which is held for sale, because it is relatively small compared to AAL’s other assets.

https://www.angloamerican.com/~/media/Files/A/Anglo-American-Group-v9/PLC/investors/investor-presentations/anglo-american-circular-notice-gm-2025.pdf

Valuation: Anglo American (LON:AAL) FY2022

IEA (2026), Mined supply and demand outlook for copper, 2026-2035, IEA, Paris https://www.iea.org/data-and-statistics/charts/mined-supply-and-demand-outlook-for-copper-2026-2035, Licence: CC BY 4.0

Teck also hold a 22.5% interest in Antamina. From Teck’s 2025 Annual Report, that interest generated gross profit of CA$1101M from 86 ktonnes of production, equivalent to a unit cost of around US$1.68/lb.